Batch Level Activities and Costs Are Incurred Again Each Time a Batch Is Produced.

3.vi Variations of Activity-Based Costing (ABC)

Learning Objective

- Aggrandize the use of activity-based costing.

Question: The primary focus of activity-based costing thus far has been on allocating manufacturing overhead costs to products. Although this is important for external reporting purposes, we can aggrandize ABC to include costs beyond manufacturing overhead. Too, we can organize costs in unlike ways to help managers evaluate operation. What unlike approaches can be used to organize price data in a manner that helps managers brand better decisions?

Answer: Cost data can be organized in a number of ways to help managers make decisions. 4 mutual approaches are addressed in this department:

- Expanding ABC to include nonmanufacturing costs

- Allocating service department costs to product departments

- Using the hierarchy of costs to organize cost data

- Measuring the costs of decision-making and failing to control quality

External Reporting and Internal Decision Making

Question: U.South. Generally Accepted Accounting Principles require the allotment of all manufacturing costs to products for inventory costing purposes. The choice of an allocation method is not critical to this process. Companies that apply direct labor hours, automobile hours, activity-based costing, or another method to allocate overhead costs to products are likely to be in compliance with U.S. GAAP. Throughout this chapter, we accept illustrated how ABC is used to allocate manufacturing overhead costs. However, organizations oftentimes use ABC for purposes that become beyond allocating costs solely for external reporting. How might ABC be used to assistance companies in areas other than external reporting?

Answer: Commissions paid to sales people for the sale of specific products (oft called selling, general, and administrative) are included equally an operating expense in financial reports prepared for external users as required by U.Due south. GAAP. Nevertheless, many organizations may assign commission costs to specific products for internal decision-making purposes. This treatment is not in compliance with U.Southward. GAAP, but it is perfectly acceptable for internal reporting purposes and may exist done using activity-based costing. Information technology is of import to empathize that managers have ultimate control over which costs should exist allocated to products for internal reporting purposes, and this allocation often involves going beyond overhead costs.

Table 3.1 "Examples of Costs Allocated to Products" provides examples of costs that could be allocated to products. It also includes cost categories—product, selling, and general and administrative (G&A)—and indicates whether the cost allocation complies with U.S. GAAP for external reporting. As y'all tin can see in the far correct column, all costs can be allocated to products for internal reporting purposes.

Table 3.1 Examples of Costs Allocated to Products

| Cost | Cost Category* | OK to Classify to Products for External Reporting (U.Southward. GAAP)? | OK to Allocate to Products for Internal Reporting? |

|---|---|---|---|

| Direct materials | Product | Yes | Yes |

| Direct labor | Product | Yes | Yes |

| Manufacturing overhead** | Product | Aye | Yes |

| Sales commissions | Selling | No | Yes |

| Shipping products to customers | Selling | No | Yeah |

| Production advertising | Selling | No | Yeah |

| Legal costs for product lawsuit | G&A | No | Yes |

| Processing payroll for product personnel | K&A | No | Yeah |

| Company president'due south salary | Grand&A | No | Yes |

| Costs of implementing ABC | Grand&A | No | Yes |

| *See Chapter ii "How Is Task Costing Used to Runway Production Costs?" for information nigh category definitions. **Includes all manufacturing costs other than straight labor and direct materials, such equally factory related costs for supervisors, building hire, automobile maintenance, utilities, and indirect materials. See Chapter 2 "How Is Job Costing Used to Runway Production Costs?" for more than detail. | |||

Allocating Service Department Costs Using the Straight Method

Question: Most companies have departments that are classified as either service departments or product departments. Service departmentsDepartments that provide services to other departments within a company. provide services to other departments within the visitor and include such functions every bit bookkeeping, human resources, legal, maintenance, and estimator support. Product departmentsDepartments directly involved with producing goods or providing services for customers. are directly involved with producing goods or providing services for customers and include such functions every bit ordering materials, assembling products, and performing quality inspections. Why do companies oft allocate a share of service department costs to product departments for internal reporting purposes even though U.S. GAAP generally does not allow it for external reporting?

Answer: Companies allocate service department costs to production departments for several reasons:

- The services provided by departments inside a visitor are not gratuitous, and they should be used as efficiently every bit possible. Managers of production departments that utilize these services thus have an incentive to minimize their use.

- To minimize costs, Hewlett Packard and other large companies often "outsource" services similar building maintenance and legal back up (i.due east., they accept other companies provide the services for them). This creates an incentive for the company'south service departments to provide services at a reasonable price.

- Organizations often include service department costs when determining product costs for internal decision-making purposes, every bit described earlier (refer to Table iii.1 "Examples of Costs Allocated to Products" for examples).

Question: How practice companies allocate service section costs to production departments and how might this be done at SailRite?

Reply: Several methods of allocating service department costs to production departments are available. We introduce the simplest approach—the straight method—here (complex approaches are presented in more than advanced price bookkeeping texts). The directly methodA method of allocating costs that allocates service department costs straight to production departments but not to other service departments. allocates service section costs directly to production departments simply non to other service departments.

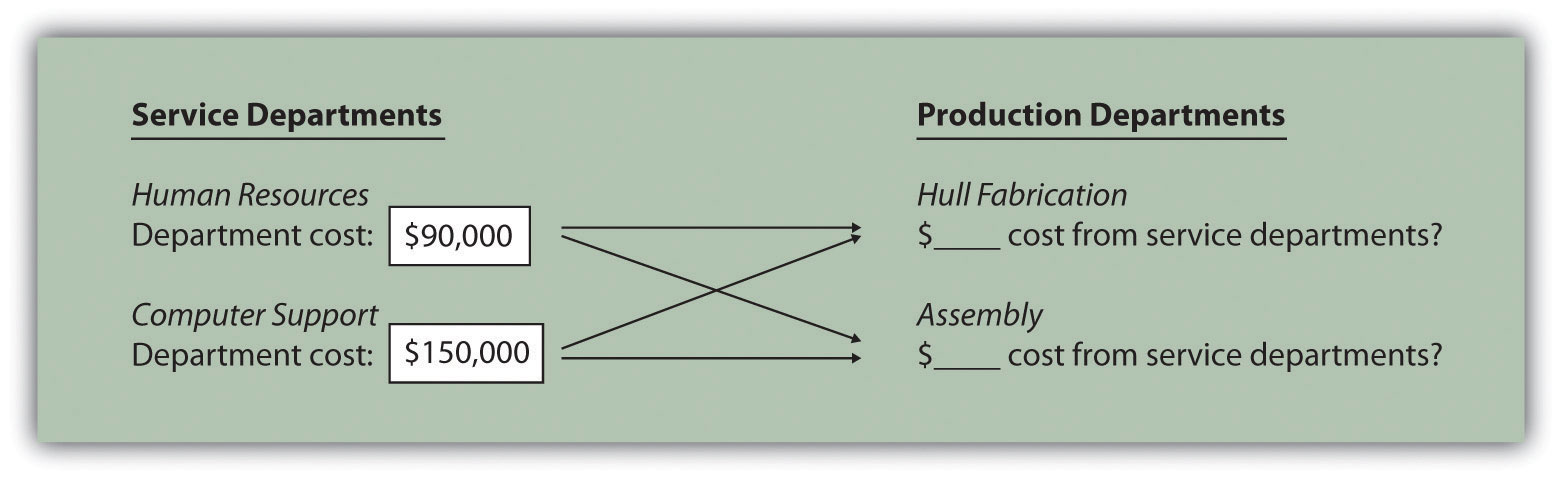

For case, assume that SailRite Visitor has two service departments—Human Resources and Computer Back up. Costs associated with Human Resources and Reckoner Support total $xc,000 and $150,000, respectively. Think that SailRite has two production departments—Hull Fabrication and Assembly. The goal is to classify service section costs to the 2 product departments, as shown in Effigy iii.10 "Allocating Service Department Costs to Product Departments at SailRite Company: Direct Method (Before Allocations)".

Effigy iii.10 Allocating Service Department Costs to Production Departments at SailRite Company: Direct Method (Before Allocations)

SailRite would similar to allocate service section costs using an allotment base that drives these costs. Assume management decides to use the number of employees as the resource allotment base to allocate Homo Resources costs, and the number of computers as the allotment base of operations to allocate Computer Support costs. Allocation base activity for each production department is equally follows:

| Hull Fabrication | Assembly | Total | |

| Number of employees | 35 | 85 | 120 |

| Number of computers | 42 | 33 | 75 |

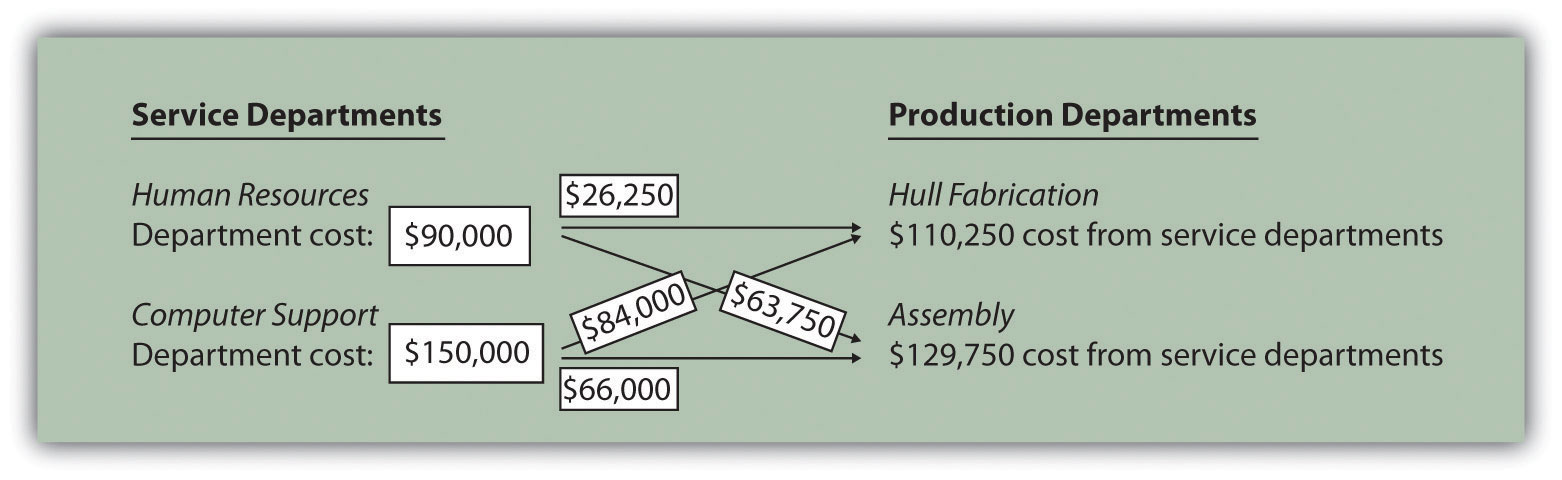

The allocation rate for human resource services is $750 per employee (= $90,000 department costs ÷ 120 employees). The allocation rate for figurer back up services is $2,000 per computer (= $150,000 ÷ 75 computers). Thus the Hull Fabrication section receives an allocation of $26,250 in human resource costs (= 35 employees × $750 charge per unit) and $84,000 in computer support costs (= 42 computers × $2,000 rate). The Assembly department receives an resource allotment of $63,750 in homo resource costs (= 85 employees × $750 rate) and $66,000 in computer support costs (= 33 computers × $ii,000 charge per unit).

The allocations to production departments are shown in Effigy iii.11 "Allocating Service Department Costs to SailRite's Product Departments: Direct Method (After Allocations)". If management chooses to allocate service department costs to production departments equally described hither, at that place must be some benefit to going through the process. Should these costs be assigned to activity toll pools for the purpose of costing products (activity-based costing)? Should product department managers be evaluated based on the utilize of these services? Should actual service department usage be compared to budgeted usage for each product department? The answers to these questions vary from i organization to the adjacent. Even so, one point is certain—the benefits of implementing this allocation system must outweigh the costs!

Figure three.11 Allocating Service Department Costs to SailRite's Production Departments: Direct Method (After Allocations)

The Hierarchy of Costs

Question: Some organizations group activities into four cost categories, called the hierarchy of costs, to assistance managers form cost pools for activity-based costing purposes. The cost bureaucracyA method of costing that groups costs based on whether the action is at the facility level, product or customer level, batch level, or unit level. Credit for developing the price hierarchy is more often than not given to R. Cooper and R. Due south. Kaplan, "Profit Priorities from Activeness-Based Costing," Harvard Concern Review, May 1991, 130–35. groups costs based on whether the activeness is at the facility level, product or customer level, batch level, or unit level. What is the deviation between each of these categories, and how does this information aid managers?

Respond: Each category inside the toll bureaucracy is described as follows:

- Facility-level activitiesActivities required to sustain facility operations and include items such as building hire and management of the mill. (or costs) are required to sustain facility operations and include items such every bit building rent and direction of the manufacturing plant. These costs are generally changed over long time horizons and are incurred regardless of how many production-, batch-, or unit of measurement-level activities have place.

- Product-level activitiesActivities required to develop, produce, and sell specific types of products. (or customer-level activities) are required to develop, produce, and sell specific types of products. This category includes items such as product development and product ad. These costs tin be changed over a shorter time horizon than facility-level activities and are incurred regardless of the number of batches run or units produced.

- Batch-level activitiesActivities required to produce batches (or groups) of products. are required to produce batches (or groups) of products and include items such as car setups and quality inspections. These costs can be changed over a shorter time horizon than production- and facility-level activities and are driven by the number of batches run rather than the number of units produced. For example, a batch can consist of producing five units or x,000 units. The costs in this category are driven by the number of batches, not the number of units in each batch.

- Unit-level activitiesActivities required to produce individual units of production, such every bit direct materials and direct labor. are required to produce private units of product and include items such every bit energy to run machines, direct labor, and direct materials. These costs can be changed over a short time horizon based on how many units management chooses to produce.

The cost hierarchy serves as a framework for managers to plant cost pools and determine what drives the change in costs for each cost pool. Information technology also provides a sense of how speedily (or slowly) costs alter based on decisions made by management. Examples of activities frequently identified past companies using activity-based costing, and how these activities fit in the cost hierarchy, appear in Table 3.2 "Cost Hierarchy Examples".

Tabular array 3.2 Price Bureaucracy Examples

| Price Hierarchy Category | Action/Price |

|---|---|

| Facility-level | Found depreciation |

| Building hire | |

| Management of facility | |

| Production/customer-level | New product development |

| Product engineering | |

| Product marketing and advertising | |

| Maintaining customer records | |

| Batch-level | Motorcar setups |

| Processing purchase orders | |

| Batch quality inspections | |

| Unit-level | Energy to run product machines |

| Direct labor | |

| Direct materials |

Measuring the Costs of Controlling and Improving Quality

Question: The bureaucracy of costs is non the simply approach organizations employ to group costs. Managers are likewise concerned well-nigh measuring the costs associated with quality. Quality-related costs can be organized into four categories. The first two categories—prevention and appraisement—are costs incurred to control and improve quality. The final two categories—internal failure and external failure—are costs incurred as a result of declining to control and amend quality. What is the difference between these cost categories, and how does this information help managers better quality?

- Prevention costsCosts for activities that prevent defects in products and services. are costs incurred to foreclose defects in products and services. Examples include designing production processes that minimize defects, providing quality training to employees, and inspecting raw materials before they are placed in production.

- Appraisal costsCosts for activities that find defective products before they are delivered to customers. (often called detection costs) are costs incurred to observe defective products before they are delivered to customers. The price of finished goods inspections falls in this category.

- Internal failure costsCosts incurred as a outcome of detecting lacking products before they are delivered to customers. are the costs incurred equally a result of detecting defective products earlier they are delivered to customers. Examples include the reworking of defective products, the scrapping of lacking products, and the auto reanimation resulting from process issues that cause defects.

- External failure costsCosts for activities that result from delivering defective products to customers. are the costs incurred as a result of delivering defective products to customers. Examples include warranty repairs, warranty replacements, and product liability resulting from unsafe defective products.

Companies that measure these costs of quality typically calculate the costs in each category equally a percent of total acquirement. The goal is to steadily shift costs toward the prevention and appraisement categories and away from the internal and external failure categories. As organizations concentrate more on preventing defects, total quality costs as a percent of acquirement tends to reject and product quality improves. Table 3.3 "Summary of Quality Costs" provides a summary of the four classifications of quality-related costs.

Table 3.3 Summary of Quality Costs

| Quality Price Category | Description |

|---|---|

| Prevention price | Cost of activities that prevent defects in products, such as quality preparation and raw materials inspections |

| Appraisal cost | Cost of activities that detect defective products before they are delivered to customers, such as finished goods inspections and field inspections |

| Internal failure cost | Cost of activities that upshot from detecting defective products before they are delivered to customers, such every bit rework and scrap |

| External failure toll | Cost of activities that event from delivering defective products to customers, such as warranty repairs and warranty replacements |

Primal Takeaway

- Activity-based costing is not simply used to classify manufacturing overhead costs to products for external reporting purposes; it is also often used to allocate selling, general, and authoritative costs to products for internal conclusion-making purposes. A number of methods tin exist used to assist in the cost allocation process. For case, the cost of service departments tin be allocated to production departments using the straight method. Also the toll hierarchy can be used to aid institute cost pools and identify cost drivers used to allocate costs. Organizations are as well concerned with measuring and reducing the toll of quality by categorizing quality costs into 4 categories—prevention, appraisal, internal failure, and external failure.

Review Problem 3.6

Make full in the following table to identify if the toll item can be included in the cost of products for external reporting purposes and/or internal reporting purposes. The first item is completed for you lot.

| Price | OK to Allocate to Products for External Reporting (U.Southward. GAAP)? | OK to Allocate to Products for Internal Reporting? |

| Straight materials | Yes | Yes |

| Salaries of sales people | ||

| Indirect materials used in production | ||

| Rent for headquarters edifice | ||

| Production promotions | ||

| Direct labor | ||

| Legal costs for patent applications | ||

| Processing payroll for homo resources personnel | ||

| Depreciation of factory equipment | ||

| Marketing vice president's bacon | ||

| Depreciation of administrative department equipment |

Solution to Review Problem 3.6

| Cost | OK to Allocate to Products for External Reporting (U.S. GAAP)? | OK to Classify to Products for Internal Reporting? |

| Straight materials | Yes | Yeah |

| Salaries of sales people | No | Yes |

| Indirect materials used in production | Aye | Yes |

| Rent for headquarters building | No | Yes |

| Production promotions | No | Yes |

| Direct labor | Yes | Yes |

| Legal costs for patent applications | No | Yep |

| Processing payroll for human resource personnel | No | Yes |

| Depreciation of factory equipment | Aye | Yes |

| Marketing vice president's salary | No | Yes |

| Depreciation of administrative department equipment | No | Yep |

Stop-of-Affiliate Exercises

Questions

- Why practice managers allocate overhead costs to products?

- Describe the three methods of allocating overhead costs.

- What is a cost pool, and how does it chronicle to allocating overhead to products?

- What is the difference between an activeness and a price driver?

- How practice cost flows using activeness-based costing differ from cost flows using 1 plantwide rate?

- Describe the v steps required to implement activity-based costing.

- What are some advantages of using an action-based costing system?

- What are some disadvantages of using an activeness-based costing organization?

- Review Annotation iii.xiv "Business organization in Action iii.1" What were the 2 common characteristics of the 130 U.S. manufacturing companies that used activity-based costing?

- Explain how to record the application of overhead to products using activity-based costing.

- Describe the three steps required to implement activity-based management.

- How does action-based management differ from activity-based costing?

-

What is the difference betwixt a value-added action and a non-value-added action? Provide ii examples of non-value-added activities for each of the following:

- Fast-food eating place

- Vesture store

- Higher bookstore

- Review Note 3.16 "Business in Action three.2" How did activeness-based costing help BuyGasCo Corporation settle its predatory pricing case?

- Review Annotation 3.23 "Business organisation in Action 3.3" What did the survey of 296 users of ABC and ABM show were the top 2 objectives in using these systems?

- Review Note 3.26 "Business in Action three.iv" What was management'south primary business organization in deciding to implement an activity-based costing system?

- What selling costs and general and administrative costs might be allocated to products using activity-based costing? Why do some managers prefer allocating these costs to products?

- What are service departments? Why do some managers allocate service department costs to product departments?

- Describe the four categories included in the hierarchy of costs.

- What is the difference between a facility-level toll and a unit-level toll?

- How does the hierarchy of costs aid managers allocate overhead costs?

- Describe the iv categories related to the costs of quality. How might the resource allotment of quality costs to these four categories help managers?

Cursory Exercises

-

Product Costing at SailRite. Refer to the dialogue presented at the beginning of the chapter and the follow-up dialogue before Figure 3.7 "Activity-Based Costing Versus Plantwide Costing at SailRite Company".

Required:

- In the opening dialogue, why was the owner concerned about the product costs for each of the company's boats?

- In the follow-up dialogue before Figure 3.7 "Action-Based Costing Versus Plantwide Costing at SailRite Company", what did the company's accountant discover about the profitability of each boat using activeness-based costing? (Refer to Effigy 3.7 "Activity-Based Costing Versus Plantwide Costing at SailRite Company" as you ready your answer.)

-

Calculating Plantwide Predetermined Overhead Rate. Manufacturing overhead costs totaling $5,000,000 are expected for this coming twelvemonth. The visitor also expects to utilise 50,000 straight labor hours and xx,000 automobile hours.

Required:

- Calculate the plantwide predetermined overhead rate using direct labor hours equally the base. Provide a i-sentence description of how the rate will be used to allocate overhead costs to products.

- Calculate the plantwide predetermined overhead charge per unit using machine hours as the base of operations. Provide a one-sentence clarification of how the rate will be used to allocate overhead costs to products.

-

Calculating Department Predetermined Overhead Rates. Manufacturing overhead costs totaling $1,000,000 are expected for this coming year—$400,000 in the Assembly department and $600,000 in the Finishing section. The Assembly section expects to use 4,000 machine hours, and the Finishing department expects to apply 30,000 direct labor hours.

Required:

- Assume this company uses the section approach for allocating overhead costs. Calculate the predetermined overhead rate for each department, and explain how these rates will be used to allocate overhead costs to products.

- Why do different departments use different allocation bases (east.grand., straight labor hours or car hours)?

-

Identifying Cost Drivers. Ehrman Company identified the activities listed in the following as being most important (step ane and step 2 of activity-based costing), and it formed cost pools for each activity.

- Purchasing raw materials

- Inspecting raw materials

- Storing raw materials

- Maintaining production equipment

- Setting up machines to produce batches of product

- Testing finished products

Required:

Perform stride 3 of the activeness-based costing process past identifying a possible cost commuter for each activity.

-

Identifying Cost Drivers: Service Company. McHale Architects, Inc., designs, engineers, and supervises the structure of custom homes. The post-obit activities were identified as being most important (step 1 and pace 2 of action-based costing), and price pools were formed for each activity.

- Meeting with customers

- Coordinating inspections with the building department

- Consulting with contractors

- Maintaining part equipment

- Processing customer billings (invoices)

Required:

Perform stride three of the activeness-based costing process by identifying a possible toll driver for each action.

-

Value-Added and Non-Value-Added Activities. Novak Corporation manufactures custom-fabricated kayaks and accessories. The visitor performs the post-obit activities.

- Storing parts and materials

- Queuing orders earlier outset production

- Assembling kayaks

- Waiting for materials to arrive to proceed production

- Painting kayaks

- Designing kayaks to maximize comfort

- Scrapping defective materials

Required:

Label each activity equally value-added or non-value-added.

-

Resource allotment Base for Service Departments. Valencia Company has xv production departments and produces hundreds of products. Service section costs are allocated to production departments using the direct method. Five service departments provide the following services to the production departments.

- The Computer Engineering department provides estimator back up.

- The Personnel department posts chore openings, hires employees, and coordinates employee benefits.

- The Bookkeeping section processes accounting data, provides financial reports, and performs full general accounting duties.

- The Maintenance department maintains buildings and equipment.

- The Legal section provides legal services.

Required:

- For each service department, provide a possible allocation base. Explicate why the base yous chose for each service department is reasonable.

- Does the direct method provide for allocations from one service department to another? Explain.

Exercises: Set A

-

Plantwide Versus Department Allocations of Overhead. San Juan Company expects to incur $600,000 in overhead costs this coming year—$100,000 in the Cutting section, $300,000 in the Associates department, and $200,000 in the Finishing department. Direct labor hours worked in all departments are expected to full forty,000 (used for the plantwide rate). The Cut section expects to use 20,000 machine hours, the Associates department expects to apply 25,000 direct labor hours, and the Finishing department expects to incur $100,000 in directly labor costs (this information will be used for section rates).

Required:

- Assume San Juan Company uses the plantwide approach for allocating overhead costs and direct labor hours as the resource allotment base. Calculate the predetermined overhead rate, and explicate how this rate will be used to allocate overhead costs.

- Assume San Juan Company uses the department approach for allocating overhead costs. Calculate the predetermined overhead charge per unit for each department, and explain how these rates will exist used to allocate overhead costs.

-

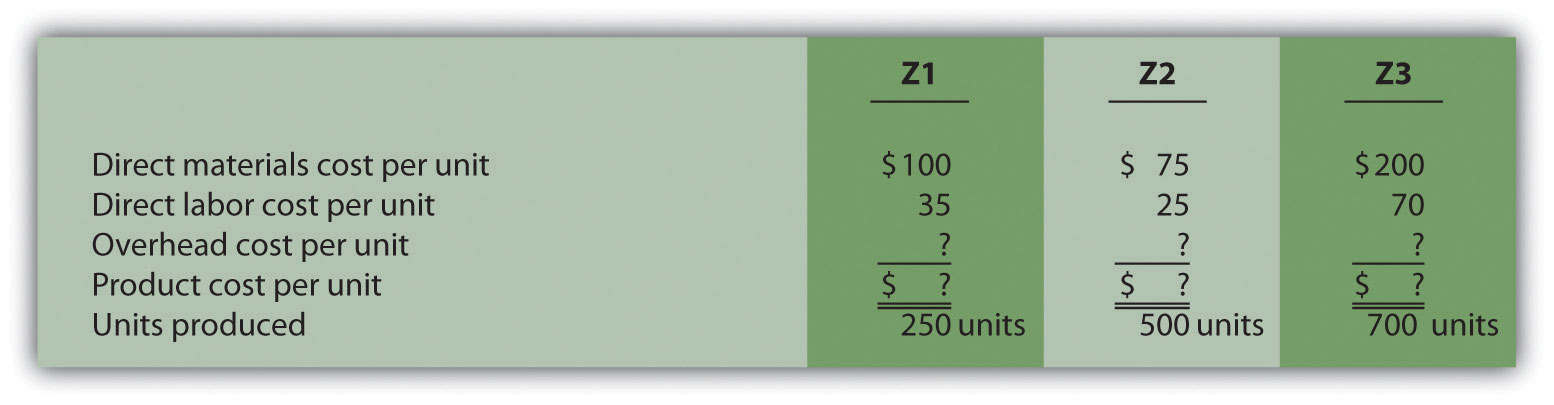

Computing Product Costs Using Activeness-Based Costing. Stillwater Company identified the following activities, estimated costs for each activity, and identified cost drivers for each action for this coming yr. (These are the first three steps of activity-based costing.)

The company produces three products, Z1, Z2, and Z3. Data well-nigh these products for the month of January follows:

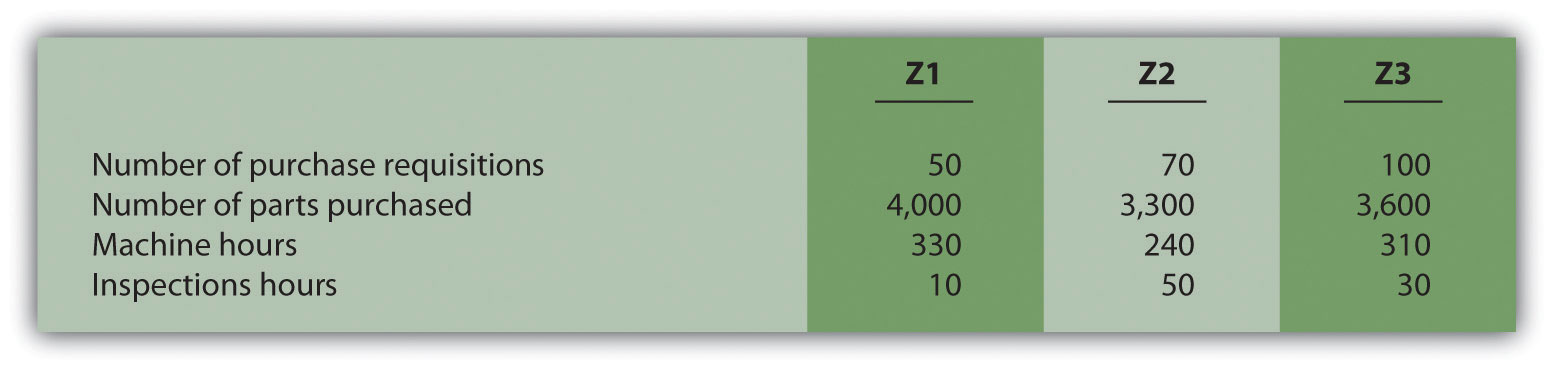

Actual cost driver activity levels for the month of January are equally follows:

Required:

- Using the estimates for the year, compute the predetermined overhead rate for each activity (this is step 4 of the action-based costing process).

- Using the activity rates calculated in requirement a and the bodily toll driver activity levels shown for January, allocate overhead to the 3 products for the month of Jan (this is step v of the activity-based costing procedure).

- For each product, calculate the overhead cost per unit of measurement for the month of Jan. Circular results to the nearest cent.

- For each production, summate the product cost per unit of measurement for the month of Jan. Round results to the nearest cent.

-

Journal Entry to Apply Overhead. Caspian Company is deciding which of iii approaches it should use to utilise overhead to products. Information for each approach is provided in the following.

- One plantwide charge per unit. The predetermined overhead charge per unit is 150 per centum of directly labor cost.

- Department rates. The Machining department uses a charge per unit of $55 per machine hour, and the Assembly department uses a rate of $35 per direct labor hr.

-

Activity-based costing rates. Three activities were identified and rates were calculated for each activity.

Purchase requisitions $15 per requisition processed Production setup $fifty per setup Quality control $lxx per inspection Required:

- Direct labor costs for the year totaled $80,000. Using the plantwide method, calculate the amount of overhead applied to products and brand the appropriate periodical entry.

- During the year, the Machining department used 1,000 machine hours, and the Assembly department used 1,200 direct labor hours. Using the section method, calculate the amount of overhead applied to products and make the appropriate journal entry.

- During the twelvemonth, 900 purchase requisitions were processed, 1,300 production setups were performed, and 400 products were inspected. Using the activeness-based costing approach, calculate the amount of overhead applied to products, and make the appropriate journal entry.

-

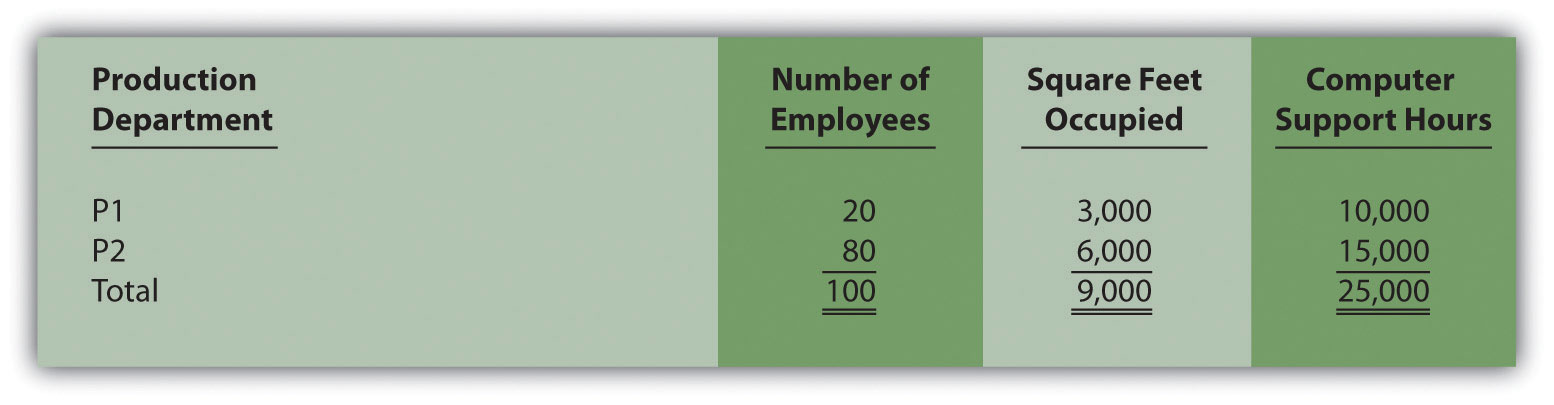

Allocating Service Department Costs. Crandall Company has two production departments (P1 and P2) and three service departments (S1, S2, and S3). Service section costs are allocated to production departments using the direct method. The $400,000 costs of department S1 are allocated based on the number of employees in each production department. The $600,000 costs of department S2 are allocated based on the square footage of space occupied past each production department. The $300,000 costs of department S3 are allocated based on hours of computer support used past each production department. Information for each production department follows.

Required:

- Calculate the service department costs allocated to each production section.

- In general, do U.Southward. Mostly Accepted Accounting Principles allow for the resource allotment of service section costs to production departments for the purpose of valuing inventory?

-

Cost Hierarchy. The following activities and costs are for Tanaka Company.

- Direct materials used by workers to gather products

- Purchase requisitions issued for raw materials

- Machines fix to produce groups of products

- New product research and evolution

- Maintenance performed on the factory building

- Straight labor assembling products

- Product designed for a specific customer

- Factory edifice rent

Required:

- Determine whether each item is a facility-level, production- or customer-level, batch-level, or unit of measurement-level price.

- Provide one example of an appropriate resource allotment base for each item. (For instance, an appropriate allocation base for detail 1 is the quantity of directly materials used.)

Exercises: Set up B

-

Plantwide Versus Department Allocations of Overhead: Service Visitor. Chan and Associates provides wetlands design and maintenance services for its customers, nearly of whom are developers. Billing is based on costs plus a 30 percent markup. Thus costs are allocated to customers rather than to products.

Total overhead costs this coming yr are expected to be $ii,000,000 ($600,000 in the Design section and $1,400,000 in the Wetlands Maintenance department). Direct labor costs are expected to total $800,000 (used for the plantwide charge per unit). The Blueprint department expects to incur direct labor costs of $500,000, and the Wetlands Maintenance department expects to piece of work thirty,000 straight labor hours (this information is used for the section rates).

Required:

- Presume Chan and Associates uses the plantwide approach to allocating overhead costs and direct labor costs as the resource allotment base. Calculate the predetermined overhead rate, and explain how this rate will exist used to allocate overhead costs. Circular results to the nearest cent.

- Assume Chan and Associates uses the section arroyo for allocating overhead costs. Calculate the predetermined overhead charge per unit for each department, and explain how these rates volition be used to allocate overhead costs. Circular results to the nearest cent.

- What are two possible interpretations of the term costs in the following statement? "Customers are billed based on costs plus a thirty percent markup."

-

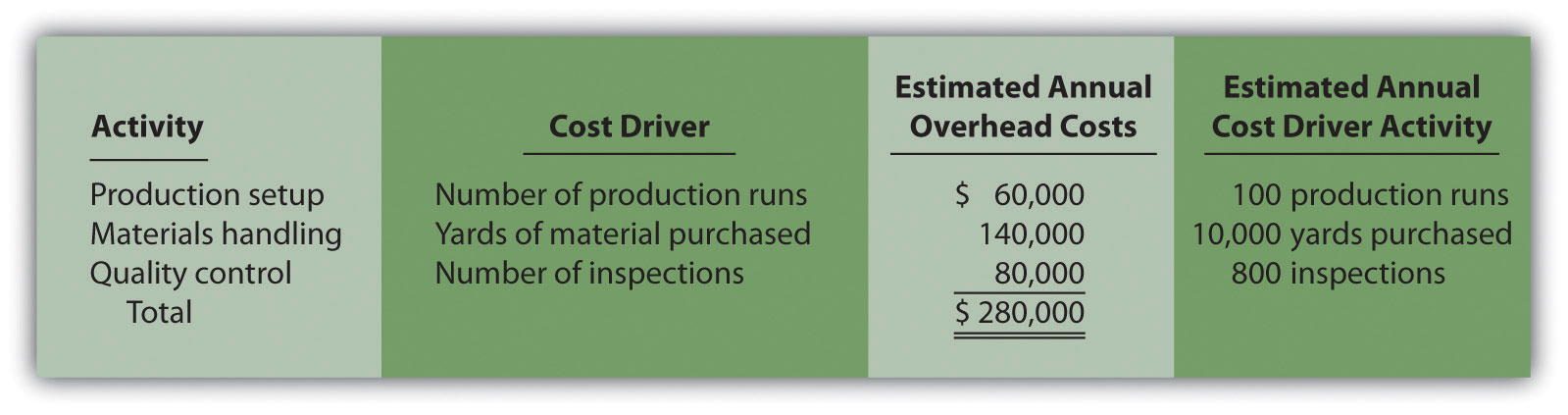

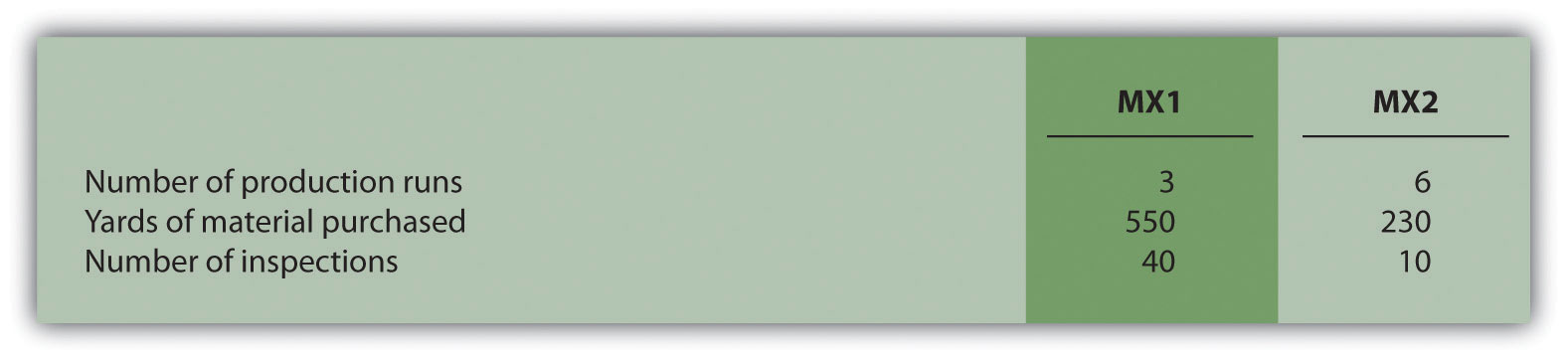

Computing Product Costs Using Activeness-Based Costing. Petrov Company identified the following activities, estimated costs for each activity, and identified cost drivers for each activeness for this coming twelvemonth. (These are the first three steps of activity-based costing.)

The company produces ii products, MX1 and MX2. Information about these products for the month of March follows:

Actual cost driver action levels for the month of March are every bit follows:

Required:

- Using the estimates for the year, compute the predetermined overhead rate for each activity (this is pace 4 of the activity-based costing process).

- Using the action rates calculated in requirement a and the actual cost driver activity levels shown for March, allocate overhead to the three products for the month of March (this is step five of the activity-based costing process).

- For each product, calculate the overhead cost per unit for the month of March. Round results to the nearest cent.

- For each product, calculate the product price per unit for the month of March. Circular results to the nearest cent.

-

Journal Entry to Use Overhead, Endmost Overhead Business relationship. Premium Products, Inc., is deciding which of three approaches information technology should use to apply overhead to products. Data for each approach is provided as follows.

- I plantwide rate. The predetermined overhead rate is $130 per direct labor 60 minutes.

- Department rates. The Cutting department uses a charge per unit of 200 percent of direct labor cost, and the Finishing section uses a charge per unit of $50 per machine hour.

-

Activity-based costing rates. Three activities were identified, and rates were calculated for each action.

Materials treatment $eight per pound of cloth purchased Product setup $60 per setup Quality command $110 per batch inspected Required:

- Direct labor hours totaled 2,000 for the yr. Using the plantwide method, calculate the amount of overhead practical to products, and make the advisable journal entry.

- During the year, the Cutting department incurred $80,000 in direct labor costs, and the Finishing department used 1,800 machine hours. Using the department method, calculate the amount of overhead applied to products, and brand the appropriate journal entry.

- During the year, 6,000 pounds of textile were purchased, 1,600 product setups were performed, and 1,300 batches of products were inspected. Using the action-based costing approach, summate the amount of overhead applied to products, and make the appropriate journal entry.

-

Premium Products, Inc., closes overapplied or underapplied overhead to the toll of goods sold account at the end of each twelvemonth. Prepare the periodical entry to close the manufacturing overhead account at the finish of the year for each of the following independent scenarios assuming the company made the journal entry to apply overhead in requirement c.

- The company recorded $302,500 in bodily overhead costs for the twelvemonth.

- The visitor recorded $243,000 in actual overhead costs for the year.

-

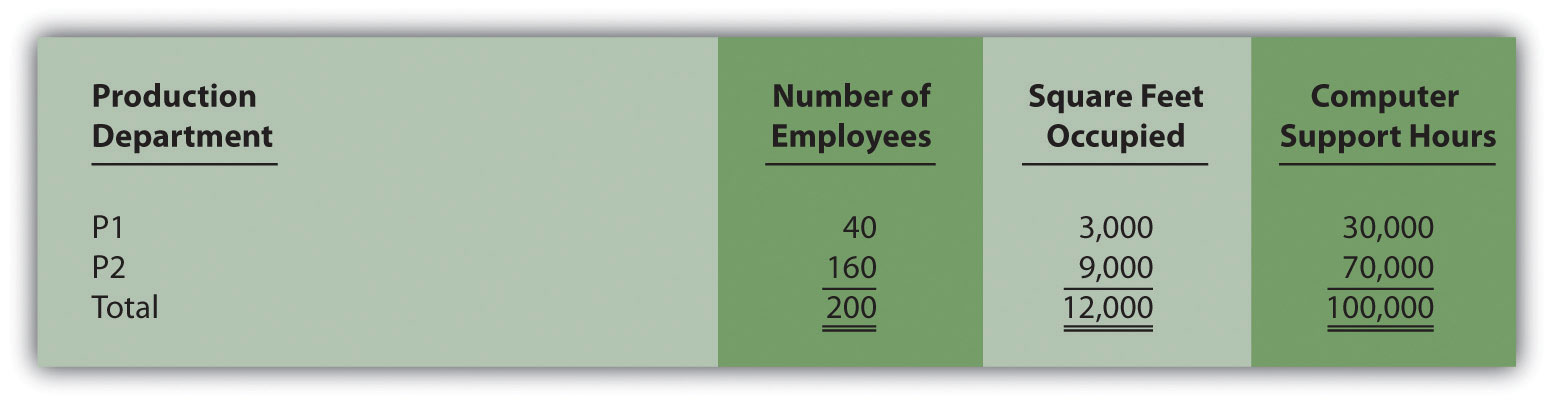

Allocating Service Department Costs. Southwest, Inc., has two production departments (P1 and P2) and three service departments (S1, S2, and S3). Service department costs are allocated to product departments using the direct method. The $800,000 costs of department S1 are allocated based on the number of employees in each product department. The $300,000 costs of department S2 are allocated based on the square footage of infinite occupied by each production department. The $600,000 costs of department S3 are allocated based on hours of estimator support used by each production department. Information for each production department follows.

Required:

- Calculate the service department costs allocated to each production section.

- In general, exercise U.S. Generally Accepted Accounting Principles allow for the allotment of service department costs to production departments for the purpose of valuing inventory?

-

Toll Hierarchy. The post-obit activities and costs are for Rios Corporation.

- Salary of a supervisor responsible for one product line

- Moving groups of products to the finished goods warehouse upon completion

- New product design

- Factory building depreciation

- Direct materials used by workers to assemble products

- Machines set up up to produce groups of products

- Product designed for a specific customer

- Maintenance performed on the manufactory edifice

Required:

- Decide whether each item is a facility-level, product- or customer-level, batch-level, or unit-level price.

- Provide ane example of an advisable allocation base for each item.

Issues

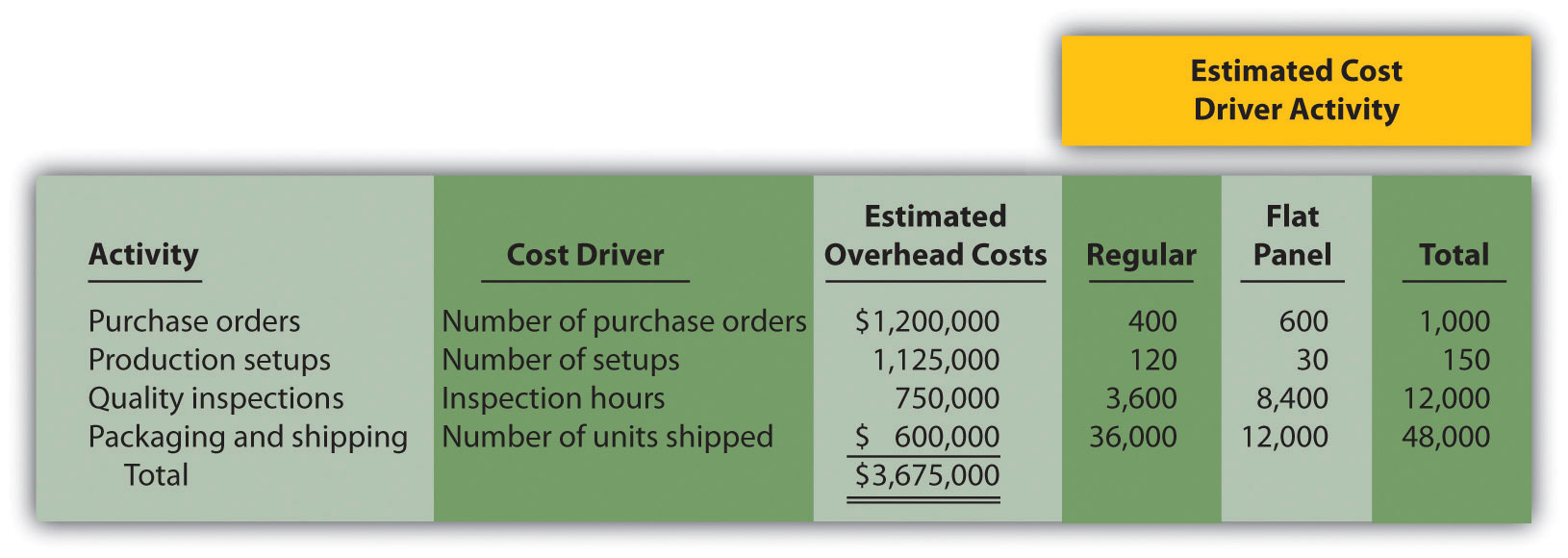

-

Activity-Based Costing Versus Traditional Approach. Techno Company produces a regular computer monitor that sells for $175 and a flat panel reckoner monitor that sells for $300. Last year, full overhead costs of $3,675,000 were allocated based on straight labor hours. A total of 63,000 straight labor hours were required last yr to build 36,000 regular monitors (i.75 hours per unit), and 42,000 direct labor hours were required to build 12,000 flat panel monitors (three.fifty hours per unit). Full direct labor and straight materials costs for last year were as follows:

Regular Monitor Apartment Console Monitor Directly materials $one,908,000 $ 900,000 Straight labor $1,728,000 $1,200,000 The direction of Techno Company would similar to use activity-based costing to allocate overhead rather than 1 plantwide charge per unit based on directly labor hours. The post-obit estimates are for the activities and related cost drivers identified as having the greatest impact on overhead costs.

Required:

- Summate the direct materials cost per unit and direct labor cost per unit for each product.

-

- Using the plantwide allocation method, calculate the predetermined overhead rate and determine the overhead toll per unit allocated to the regular and flat panel products.

- Using the plantwide allocation method, summate the production price per unit for the regular and flat console products. Round results to the nearest cent.

-

- Using the activeness-based costing allocation method, summate the predetermined overhead rate for each activity. (Hint: Step one through footstep iii in the activity-based costing process have already been done for you lot; this is footstep iv.)

- Using the activity-based costing allocation method, allocate overhead to each product. (Hint: This is pace 5 in the activity-based costing process.) Decide the overhead cost per unit. Circular results to the nearest cent.

- What is the product cost per unit for the regular and flat console products?

- Calculate the per unit of measurement turn a profit for each product using the plantwide approach and the activity-based costing approach.

- How much did the profit per unit alter for each product when moving from the plantwide approach to the activity-based costing approach? What caused this modify?

-

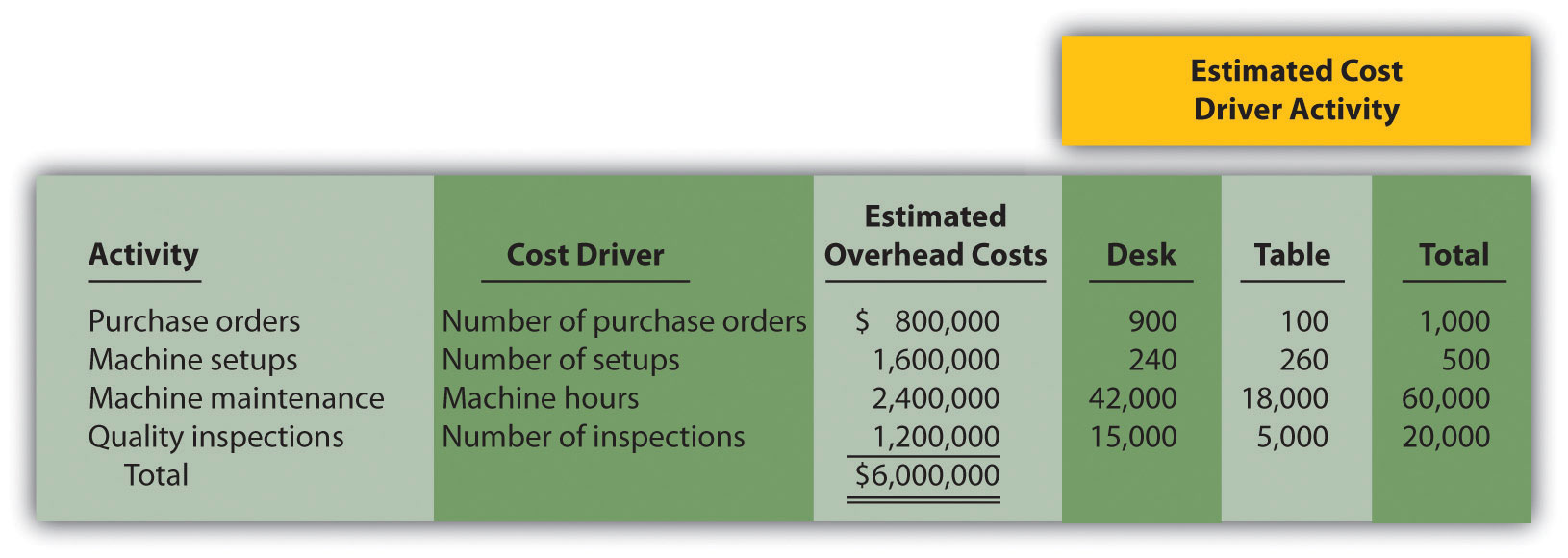

Activity-Based Costing Versus Traditional Arroyo, Activeness-Based Management. Quality Furniture, Inc., produces a forest desk-bound that sells for $500 and a wood table that sells for $900. Last year, total overhead costs of $6,000,000 were allocated based on directly labor costs. Direct labor costs totaled $two,000,000 last year, and Quality Furniture produced xv,000 desks and 5,000 tables. Total directly labor and straight materials costs past product for last year were as follows:

Desk Table Direct materials $1,575,000 $950,000 Direct labor $1,200,000 $800,000 The direction of Quality Furniture would like to apply activity-based costing to classify overhead rather than one plantwide charge per unit based on directly labor costs. The following estimates are for the activities and related cost drivers identified as having the greatest impact on overhead costs.

Required:

- Calculate the direct materials price per unit and directly labor toll per unit for each product.

-

- Using the plantwide allocation method, summate the predetermined overhead rate and determine the overhead cost per unit of measurement allocated to the desk and table products.

- Using the plantwide allocation method, summate the product cost per unit for the desk and tabular array products. Round results to the nearest cent.

-

- Using the activity-based costing allotment method, summate the predetermined overhead rate for each activity. (Hint: Footstep 1 through step 3 in the activity-based costing procedure have already been done for yous; this is pace 4.)

- Using the activity-based costing allocation method, classify overhead to each production. (Hint: This is pace 5 in the activity-based costing process.) Decide the overhead cost per unit. Round results to the nearest cent.

- What is the product price per unit of measurement for the desk and table products?

- Calculate the per unit turn a profit for each product using the plantwide arroyo and the activity-based costing approach. How much did the per unit profit change when moving from one approach to the other?

- Refer to the estimated cost driver action provided. Calculate the percent of each activeness consumed past each production (e.1000., the desk product issued 900 of the i,000 purchase orders issued in total and therefore consumes 90 per centum of this activity). These percentages represent the amount of overhead costs allocated to each production using activity-based costing. Using the plantwide approach, 60 percent of all overhead costs are allocated to the desk-bound and twoscore percent to the tabular array. Compare the activity-based costing percentages to the percentage of overhead allocated to each product using the plantwide arroyo. Utilise this data to explicate what caused the shift in overhead costs to the desk product using activity-based costing.

-

Calculating and Recording Overhead Practical. Assume Quality Piece of furniture, Inc., discussed in Problem 41, uses activity-based costing.

Required:

- Using the data presented at the outset of Problem 41, summate the predetermined overhead rate for each activity.

-

The following activity associated with the desk-bound production was reported for the month of March.

Number of buy orders processed 40 Number of machine setups 22 Number of machine hours 2,425 Number of quality inspections 890 Using the predetermined overhead rates calculated in requirement a, decide the amount of overhead applied to the desk product for the month of March.

- Make the journal entry to record overhead applied to the desk product for the month of March.

- Assume you are the manager of the desk production line and would like to reduce the amount of overhead costs being applied to your products. Which activity would you focus on first? Why?

-

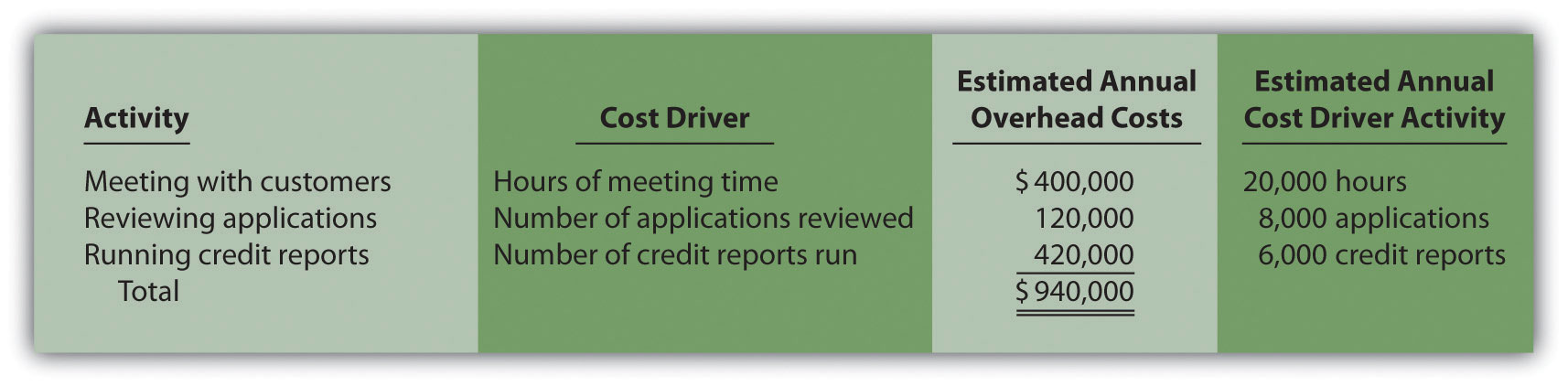

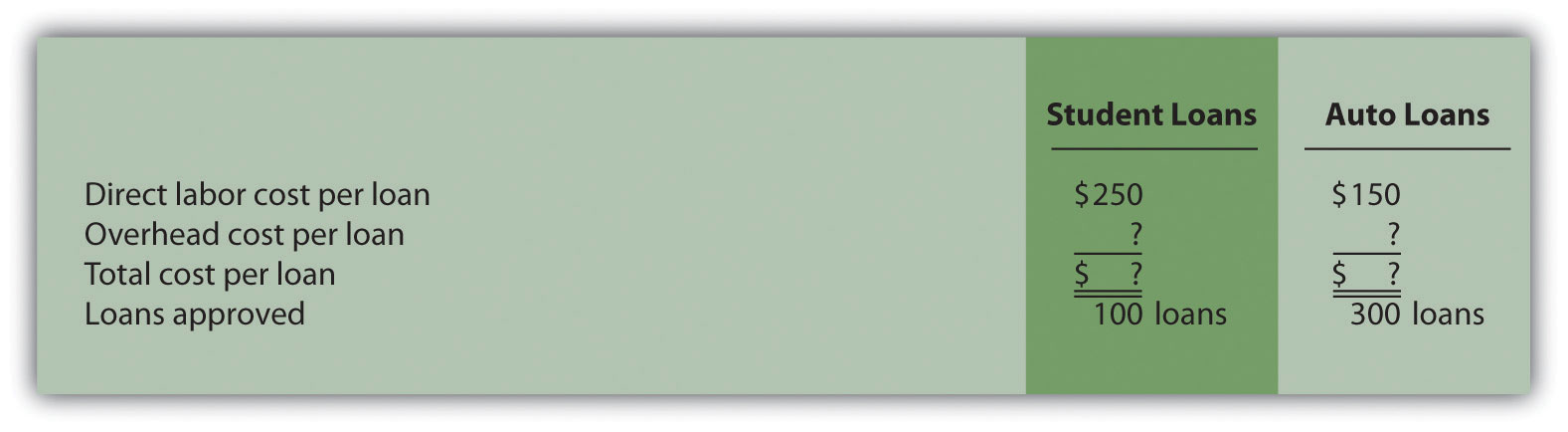

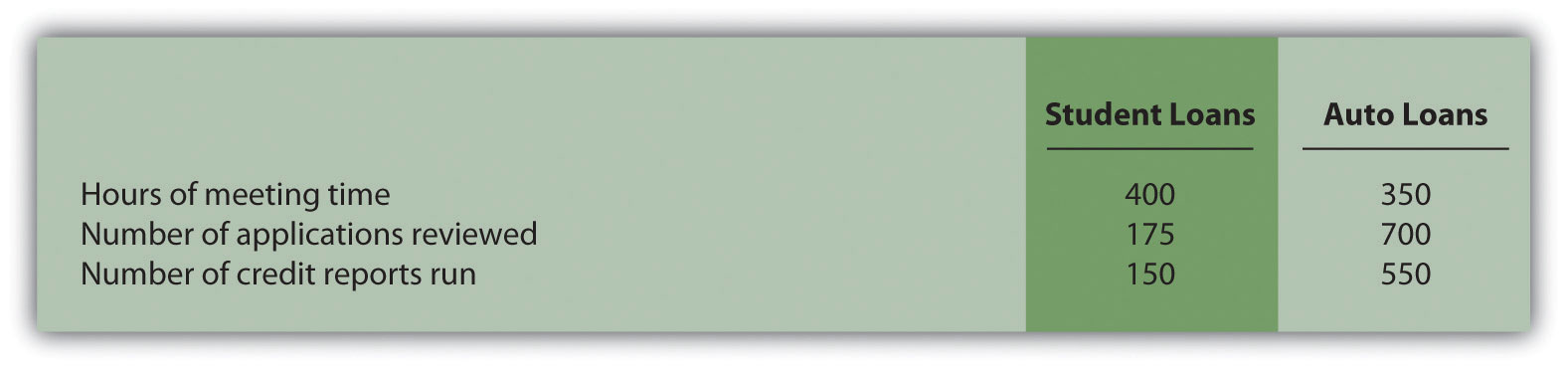

Computing Product Costs Using Activity-Based Costing, Service Visitor. Roseville Community Bank uses activeness-based costing to assign overhead costs to two different loan products—student loans and auto loans. The bank identified the following activities, estimated costs for each activity, and identified cost drivers for each activity for this coming year. (These are the first 3 steps of activity-based costing.)

The following information for the ii loan products offered past Roseville Customs Bank is for the calendar month of July:

Actual cost commuter activity levels for the month of July are as follows:

Required:

- Using the estimates for the year, compute the predetermined overhead rate for each activity (this is step 4 of the activity-based costing process).

- Using the activity rates calculated in requirement a and the actual cost commuter activity levels shown for July, classify overhead to the two products for the month of July.

- For each loan product, calculate the overhead cost per loan approved for the month of July. Round results to the nearest cent.

- For each loan product, calculate the total toll per loan approved for the month of July. Circular results to the nearest cent.

- Assume you lot are the manager of the auto loans product line and would like to reduce the amount of overhead costs being applied to your products. Which activity would you lot focus on first? Why?

-

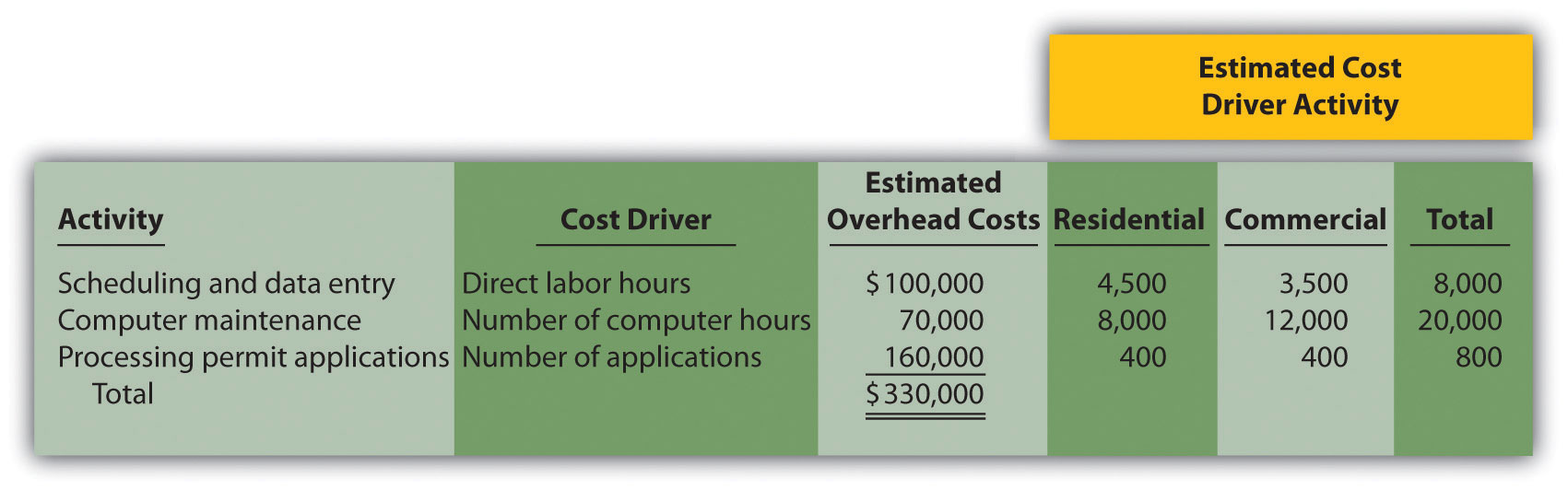

Activity-Based Costing Versus Traditional Approach: Service Company, Activeness-Based Management. Hodges and Associates is a small house that provides structural engineering services for its clients. The company performs structural engineering science services for both residential and commercial buildings. Concluding twelvemonth, total overhead costs of $330,000 were allocated based on straight labor costs. A total of $300,000 in straight labor costs were incurred in the following areas: $120,000 in the residential segment and $180,000 in the commercial segment. Direct materials used were negligible and are included in overhead costs. Sales revenue totaled $450,000 for residential services and $330,000 for commercial services.

The management of Hodges and Associates would like to use activeness-based costing to allocate overhead rather than a plantwide rate based on direct labor costs. The following estimates are for the activities and related toll drivers identified as having the greatest bear on on overhead costs.

Required:

-

- Using the plantwide allocation method, summate the full price for each production. (Hint: Product costs for this company include overhead and direct labor.)

- Using the plantwide approach, calculate the profit for each production. Also calculate profit equally a percent of sales revenue for each production (circular to the nearest tenth of a percent).

-

- Using activity-based costing, calculate the predetermined overhead rate for each action. (Hint: Footstep 1 through footstep 3 in the action-based costing process take already been done for yous; this is stride 4.) Round results to the nearest cent.

- Using activity-based costing, calculate the amount of overhead assigned to each product. (Hint: This is step five in the activity-based costing process.)

- Using activity-based costing, calculate the profit for each product. Also calculate profit as a pct of sales revenue for each product (round to the nearest tenth of a percent).

- What caused the shift of overhead costs to the residential product using activity-based costing? How might direction use this information to brand improvements within the company?

-

-

Calculating and Recording Overhead Applied: Service Company. Presume Hodges and Associates, discussed in Problem 44, uses activity-based costing.

Required:

- Using the data presented at the beginning of Problem 44, calculate the predetermined overhead rate for each activity. Circular results to the nearest cent.

-

The following activity associated with the commercial product was reported for the calendar month of September.

Number of direct labor hours 350 Number of reckoner hours 960 Number of applications 50 Using the predetermined overhead rates calculated in requirement a, determine the amount of overhead practical to the commercial product for the month of September.

- Make the journal entry to record overhead applied to the commercial production for the calendar month of September.

- Assume yous are manager of the commercial product line and would like to reduce the amount of overhead costs existence applied to your products. Which activity would you lot focus on first? Why?

-

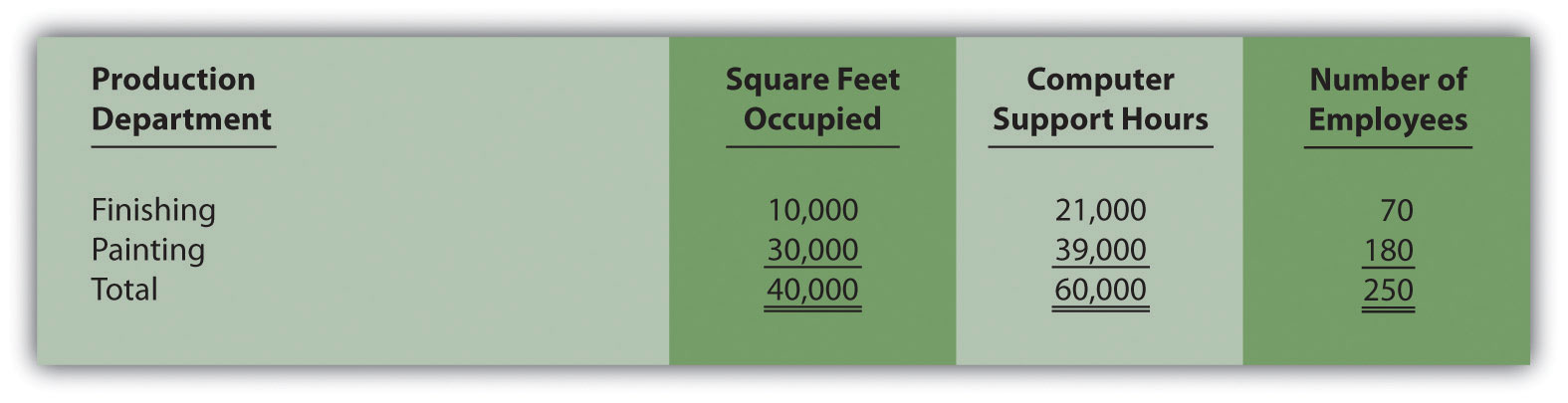

Allocating Service Department Costs. Szabo Industries has two product departments (Finishing and Painting) and three service departments (Maintenance, Calculator Support, and Personnel). Service department costs are allocated to production departments using the direct method. Maintenance allocates costs totaling $3,000,000 based on the foursquare footage of space occupied by each product department. Computer Back up allocates costs totaling $iv,000,000 based on hours of computer support used by each production department. Personnel allocates costs totaling $2,500,000 based on number of employees in each product department. Information for each production department follows.

Required:

- Calculate the service department costs allocated to each production department.

- Why exercise companies allocate service department costs to production departments?

-

Selecting an Allocation Base of operations for Service Costs. Winstead, Inc., is looking for an appropriate resource allotment base to allocate personnel costs totaling $5,000,000. Service department costs are allocated to iii production departments: Assembly, Sanding, and Finishing. Management is because two allotment bases.

Possible Allocation Base Assembly Sanding Finishing Number of employees 30 20 fifty Square anxiety of space occupied 25,000 15,000 ten,000 Required:

- Calculate the amount of personnel section costs allocated to production departments using each resource allotment base of operations.

- Which allocation base practise you think is near reasonable? Why?

One Step Further: Skill-Building Cases

-

Overhead Allotment. Do you agree with the following statement? Explain your answer.

Total estimated overhead costs will vary depending on whether we use the plantwide method, section method, or activity-based costing to allocate overhead.

-

Cost Allocation Problems. Assume you rent a firm with 2 friends. The total monthly rent is $ane,500. Your bedroom is the smallest of the three bedrooms, and each of the others has a bath attached. You lot and your friends are trying to decide how to divide upward the rent. Two possibilities are being discussed.

- Share the cost equally amid the iii of yous.

- Make up one's mind rent based on square feet occupied (the fastened bathrooms would be part of the foursquare footage measurement).

Required:

- Which approach exercise yous recollect is near off-white for all involved? Why?

- Which approach is easiest? Why?

- Advise another approach to dividing upwardly the cost of rent.

- Action-Based Costing and Activity-Based Direction. A colleague states, "Nosotros produce i production, and our operations are relatively uncomplicated. Activity-based costing and activity-based management would be a waste of fourth dimension for our visitor!" Do you agree with this statement? Explicate.

- Product Costs. The visitor president makes the following argument: "Product costs are straightforward. Whatever costs are incurred to produce a product are assigned to that product." Do you agree with this statement? Explain.

-

Changing Plantwide Resource allotment Charge per unit at SailRite. Recall from the affiliate discussion that SailRite uses one plantwide rate based on direct labor hours to allocate manufacturing overhead costs to the company's two sailboat products—Bones and Deluxe. Management was concerned almost the inaccuracy of overhead costs being assigned to each product and decided to calculate product costs using activity-based costing. Production price and profit results are summarized in the post-obit for the plantwide resource allotment approach (based on direct labor hours) and activity-based costing approach. This information was presented in the chapter in Figure 3.7 "Activity-Based Costing Versus Plantwide Costing at SailRite Company".

Although management of SailRite prefers the accuracy of activity-based costing, the price of maintaining such an accounting organisation for the long term is prohibitive. John, the accountant, has proposed going back to using one plantwide charge per unit, but he would like to allocate overhead costs using car hours rather than direct labor hours.

Call back that overhead costs totaled $8,000,000. A full of 90,000 machine hours were used for the period: 50,000 for Basic sailboats and forty,000 for Deluxe sailboats. The company produced 5,000 units of the Bones model and 1,000 units of the Palatial model. Thus the Basic model uses 10 machine hours per unit (= 50,000 auto hours ÷ 5,000 units) and the Deluxe model uses 40 machine hours per unit (= 40,000 automobile hours ÷ 1,000 units).

Required:

- Calculate the predetermined overhead charge per unit using machine hours as the allocation base, and make up one's mind the overhead cost per unit allocated to the Bones and Deluxe sailboats. Round results to the nearest cent.

- For each production, summate the unit of measurement production cost and profit using the same format presented previously. Round results to the nearest cent.

- Compare your results in requirement b to the results using direct labor hours every bit the allotment base of operations and activeness-based costing.

- Provide at least two reasons why management might prefer machine hours as the overhead allocation base rather than direct labor hours or activity-based costing.

-

Service Department Cost Allocation. Biotech, Inc., recently began providing cafeteria services to its employees. Because revenue from the sale of food at the cafeteria does not fully cover deli expenses, Biotech must pay for the shortfall. These costs are allocated to production departments based on employee usage. That is, the company tracks which employees use the cafeteria and allocates costs to product departments appropriately.

Sarah Kolster, manager of the quality testing department, is not happy with receiving cafeteria toll allocations. She is evaluated based on meeting a cost budget established at the kickoff of the fiscal year, which does not include the deli allocation, and she clearly has an incentive to minimize costs.

When Sarah met with the company's accountant, Dan, regarding this issue, she said, "Dan, I like the thought of providing cafeteria service to our employees, but the costs allocated to my section are killing my budget. Last calendar month alone, I was allocated $3,000 in costs related to the new cafeteria. I accept no choice but to require my employees to go elsewhere for food."

Dan responded, "I sympathise your concern, Sarah. Management's intent was to provide a service to our employees that would improve productivity and advantage employees for their hard work. If you tell your employees to stop using the cafeteria, more costs will be allocated to other departments, and the other departments might also end using the deli. My conventionalities is that the cafeteria will be self-sufficient inside a year if more than employees are encouraged to use it. This translates into no more toll allocations to departments within a year. I'll hash out your concerns with top direction later on this week."

Required:

- Why does Biotech, Inc., allocate cafeteria costs to departments?

- What recommendations would you brand to top management regarding the way cafeteria costs are allocated to departments?

Comprehensive Case

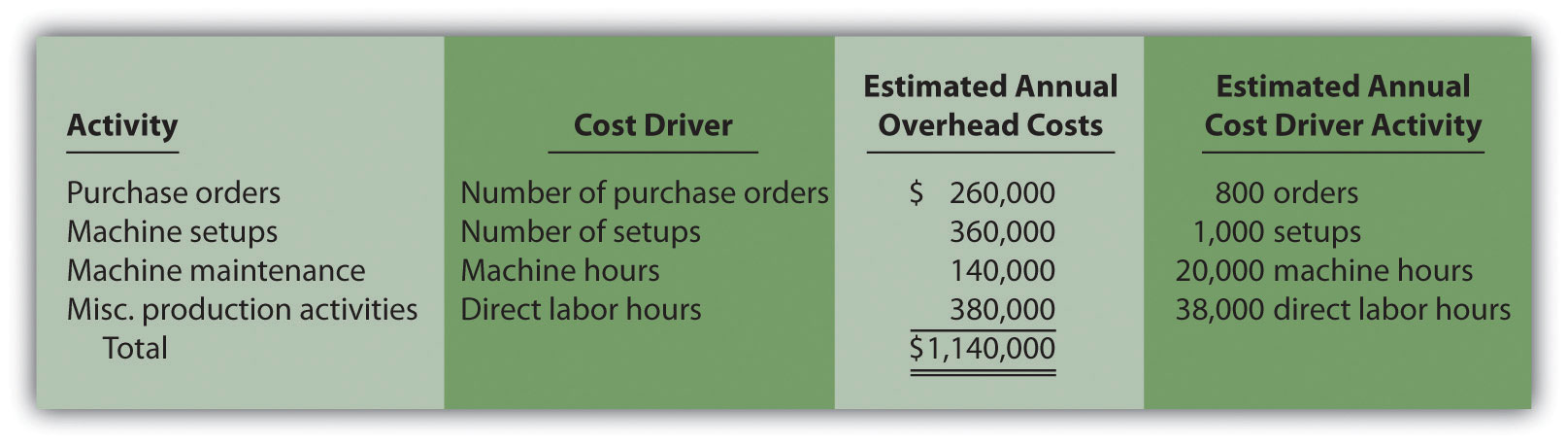

-

Activity-Based Costing, Periodical Entries, T-Accounts, and Preparing an Income Statement. This trouble is an adaptation of the instance presented at the stop of Affiliate ii "How Is Job Costing Used to Rail Production Costs?" for Custom Furniture Company. The only divergence is that this problem uses activity-based costing to allocate overhead costs rather than i plantwide rate. Call up that inventory start balances were $25,000 for raw materials inventory, $35,000 for work-in-procedure inventory, and $90,000 for finished goods inventory.

Direction of Custom Furniture Company would like to use activity-based costing to allocate overhead costs totaling $i,140,000 rather than one plantwide charge per unit based on direct labor hours. The following estimates are for the activities and related toll drivers identified as having the greatest impact on overhead costs.

Transactions for the month of May are shown every bit follows:

- Raw materials were purchased during the calendar month for $xv,000 on account.

- Raw materials totaling $21,000 were placed in product: $3,000 for indirect materials (gum, screws, nails, and the similar) and $18,000 for direct materials (woods planks, hardware, etc.).

- Timesheets from the straight labor workforce show total costs of $40,000, to be paid the next month.

- Production supervisors and other indirect labor working in the mill are owed wages totaling $27,000.

- The following costs were incurred related to the factory: building depreciation of $29,000, insurance of $xi,000 (originally recorded as prepaid insurance), utilities of $4,000 (to exist paid the next calendar month), and maintenance costs of $22,000 (paid immediately).

-

Manufacturing overhead is practical to products based on the following cost driver activity for the month:

Number of buy orders 75 Number of auto setups 120 Machine hours 1,850 Direct labor hours 3,240 - The post-obit selling costs were incurred: wages of $5,000 (to be paid the next month), building hire of $3,000 (originally recorded as prepaid rent), and ad totaling $10,000 (to be paid the next month).

- The following general and administrative (Grand&A) costs were incurred: wages of $13,000 (to be paid the side by side month), equipment depreciation of $6,000, and building rent of $7,000 (originally recorded every bit prepaid rent).

- Completed goods costing $155,000 were transferred out of work-in-process inventory.

- Sold goods for $100,000 on account and $90,000 cash.

- The goods sold in the previous transaction had a toll of $129,000.

- Closed the manufacturing overhead account to cost of appurtenances sold.

Required:

- Summate the predetermined overhead rate for each activity.

- Prepare T-accounts for the post-obit accounts: cash, accounts receivable, prepaid insurance, prepaid rent, raw materials inventory, work-in-procedure inventory, finished goods inventory, accumulated depreciation (building and equipment), accounts payable, wages payable, manufacturing overhead, sales, cost of goods sold, advertising expense (selling), rent expense (selling), wages expense (selling), depreciation expense (Thou&A), rent expense (G&A), and wages expense (G&A). Enter kickoff balances in T-accounts for the inventory accounts (raw materials, work in process, and finished goods).

- Prepare a journal entry for each of the transactions 1 through eleven, and mail each entry to the T-accounts fix in requirement b. Label each entry in the T-accounts past transaction number, and total each T-account.

- Is overhead underapplied or overapplied for the calendar month of May? Based on the balance in the manufacturing overhead T-business relationship prepared in requirement c, prepare a periodical entry for transaction 12.

- Fix an income statement for the month of May. (Hint: Exist sure to include the adjustment made to price of appurtenances sold in requirement d.)

Source: https://saylordotorg.github.io/text_managerial-accounting/s07-06-variations-of-activity-based-c.html

0 Response to "Batch Level Activities and Costs Are Incurred Again Each Time a Batch Is Produced."

Enregistrer un commentaire